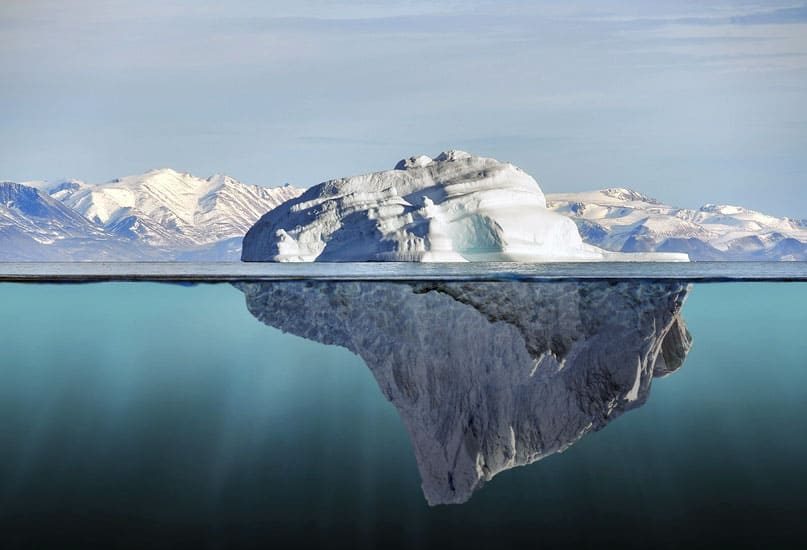

We call pricing strategy the “iceberg” of business value. The iceberg analogy conjures up images of ships going down in the night and polar bears drifting in the Atlantic. But we not talking about a Hollywood blockbuster or National Geographic documentary. We are talking about the highly leveraged effect that top line pricing strategy has on the bottom line of a company.

Pricing Math and the Magical Shrinking Earnings Problem

As we’ve discussed before, experience across thousands of companies shows that changes in price impact EBITDA by an average of 10-12X. That means every 2% change in a company’s pricing without a volume change normally yields a 25% change in EBITDA. (These numbers can vary, but for traditional companies like retailers, manufacturers, large professional service firms, etc. the variance is fairly minimal.)

Take a look at this shrinking earnings problem in action at a fictitious aftermarket auto parts manufacturer with $240 million in annual sales.

Here is what happens in a typical customer deal:

- List Price of shipment = $10,000

- LESS: 15% volume discount = -$1,500

- Discounted Price = $8,500

- LESS: Cost of Goods Sold = -$6,000

- Gross Margin = $2,500

- LESS: Operating Expenses = $1,500

- Operating Income of this shipment = $1,000

- Operating Margin of this shipment = 11.8%

On first glance, an operating margin of 11.8% appears moderately healthy compared to market comps. But is the company’s pricing strategy truly optimal? Or is management leaving significant value on the table without knowing it and short-changing the shareholders?

To know if the price is optimized you need to do two things:

STEP 1: Analyze top-line pricing of this product across the firm’s customers (and the industry if the data is available).

In this step, analyze whether pricing is consistent and fair across similar customers buying similar products at similar volumes. Your goal is to discover if there is pricing integrity across similar accounts, and if not, any opportunities to increase the effective price to generate greater profits.

As shown below, analyzing a sample of transactions for this product in the same volume range and geographic area uncovered an opportunity. The volume-discounted price of this transaction was $85 per unit (blue line). In this sample, there were 5 transactions below $85 and 17 transactions above $85 averaging $87.45 per unit (green line).

By increasing price by $2.45 per unit (+2.9%) to more closely reflect fair market pricing, the company would gain an additional $245 in operating profit

STEP 2: Drill down and look for hidden pricing opportunities.

These indicate pricing changes that can be made to the firm’s commercial strategy which can yield multiples of value. When you analyze this transaction, you will find the following pricing opportunities:

Cost of Goods Sold:

- Rush Order = $250

- Last minute change order = $100

These two hidden costs have reduced the operating profit for this transaction by $350.

Unnecessary rush orders can be eliminated by improved scheduling or constraining Sales from “throwing it in for no charge”. Alternatively, the customer can be charged an additional rush order fee. Likewise, any last minute change orders can be prevented or up-charged.

We have found that customers are generally willing to pay rush order charges if the speed of delivery is essential to their business at that point in time. For example, if their production line will be forced to go idle otherwise. If not, customers tend to avoid the additional cost and accept a less-urgent delivery.

If a sudden change order is necessary to their business, customers typically accept the additional change order fee. Otherwise, they will stick with the original order. Accepting last-minute change orders without passing the additional cost on to the customer can, therefore, be eliminated.

By charging for or eliminating these two hidden costs, the company would earn an additional $350 profit on this transaction and all future similar transactions.

The “Iceberg Effect” In Action

Let’s add up the numbers we get from optimizing pricing on this transaction.

- 2.9% Increase in top-line Price per Unit = $8,500 + ($2.45 x 100 units) = $8,745

- Reduction in Cost of Goods Sold: $6,000 – $350 = $5,650

- Increase in Operating Income: $1,000 + $595 = $1,595

- New Operating Margin of this shipment = 18.2%

As you can see, a 2.9% increase in unit price and $350 change in hidden costs created an additional $595 in operating profit on one shipment alone.

Operating margin rose from 11.8% to 18.2%. Optimizing top-line pricing increased operating margin by 24.5%. Eliminating hidden costs was responsible for another 35% increase.

Cascading these pricing strategy improvements across all of the company’s commercial activity has a substantial potential cumulative effect on the cash flows and valuation of the firm:

- Revenue increases 2.9% from $240 to $247 million

- Cost of Goods Sold decreases 5.8% from $169.4 to $159.5 million

- Gross Margin increases 23.9% from $70.6 to $87.4 million

- Operating Expenses stay the same

- Operating Income increases 59.7% from $28.2 to $45.1 million

Assuming a 10X EBITDA multiplier in this simple example, the potential value of the firm would increase from $282 million to $451 million. We are not saying companies will capture this amount every time they undertake a Pricing Transformation, but we can say with confidence that Private Equity firms can reliably realize a substantial improvement to business value by undergoing a pricing strategy transformation. The key is to uncover the “iceberg” and take appropriate measures to extract this value.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}